Should Aussie Expats Invest Through Trusts or Companies?

This is a blog written based on an interview conducted by Tim with Tristan, an expat tax accountant. If you’d like to watch the video, click here.

When it comes to structuring your investments as an Australian expat, one of the most common questions we hear is: Should I be using a trust or a company? In episode five of the Expat Education series, Tim Raes (Founder of Aussie Expat Home Loans) sits down with tax expert Tristan Perry (Managing Director, Tax & Accounting at RP Private) to explore this very topic—and the answer, as always, depends on your goals, where you’re living, and how you plan to invest.

Let’s unpack the key points discussed in the video and offer additional context to help you make informed decisions.

Why Use a Trust or Company in the First Place?

In Australia, discretionary trusts and companies are popular tools for structuring investments—especially for families with multiple income streams or asset protection needs.

Trusts are particularly common. As Tristan notes, “Every slightly sophisticated family in Australia who's got a few investments or properties have probably got one.” Trusts allow income distribution to beneficiaries—often other family members—based on their marginal tax rates. This was historically used for “income splitting” to reduce tax bills.

However, as Tim points out, “A lot of those rules have changed, especially around distributing to minor children.” Today, distributions to kids under 18 are heavily taxed, and even adult children need to actually receive the funds for it to be legitimate in the eyes of the ATO.

Meanwhile, companies are sometimes used for retaining profits within a structure, but they don’t get the same capital gains discounts and are typically less relevant for expats unless used for specific business purposes.

Asset Protection & Estate Planning: The Real Reasons Trusts Still Matter

Tim highlights another key motivation: asset protection. Trusts (especially those with corporate trustees) can separate personal liability from asset ownership, a strategy often used by business owners concerned about litigation.

“The most common reason people use trusts now is for asset protection... removing their assets from their personal name.”

Tristan adds that using a corporate trustee—instead of acting as an individual trustee—provides a stronger legal wall. “It’s a bit more expensive, but offers far more protection if things go south.”

The Downside: Negative Gearing and ‘Trapped’ Losses

Here's the kicker for expat investors: if you’re negatively gearing a property held in a trust, those losses often get trapped in the trust. You can't offset them against your personal income, which is a major disadvantage if you're looking for near-term tax benefits.

“You might lose half of it,” says Tristan, referring to lost benefits when income can’t be distributed efficiently. “That’s generally one of the biggest considerations.”

So while trusts can protect your assets, they may work against you if you're relying on tax deductions tied to property expenses.

Offshore? The Rules Change—And So Should Your Strategy

For Aussie expats living in places like Singapore or Hong Kong, many of the usual reasons to use a trust or company simply don’t apply.

In jurisdictions with no capital gains tax and no tax on dividends, the extra complexity of a trust may not be worth it. As Tristan says, “You start with a position of no tax on the investment earnings... the need for a trust falls away quickly.”

That said, trusts can play a role as you plan for your return to Australia. Setting one up before you repatriate can allow you to “rebase” your investments and establish a more tax-efficient structure onshore.

The Resident Director Catch (That Could Trip Up Your Loan)

One practical challenge that’s often overlooked is the resident director requirement.

If you're setting up a corporate trustee from overseas, Australian law requires that the company have at least one resident director. That usually means nominating a family member or advisor in Australia—but here’s where lending gets tricky.

“Almost every lender will want a personal guarantee from every director,” Tim warns. “That means mum or dad might need to be involved in your loan application. And they might not be too keen on that.”

This often becomes a stumbling block for expat borrowers, and in many cases, can derail an otherwise solid loan application.

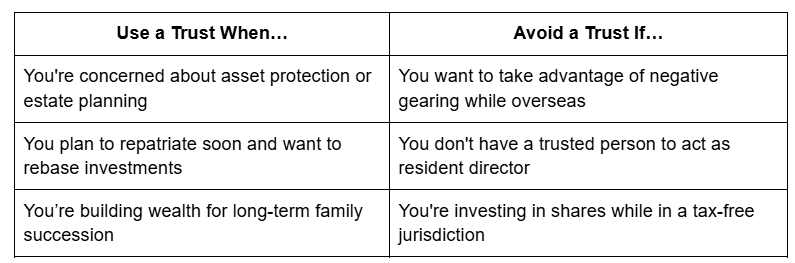

So... Should You Use a Trust or Not?

There’s no one-size-fits-all answer, but here are some guidelines based on the discussion:

As Tristan summarises: “In the majority of cases where clients ask about trusts, we conclude it’s probably not a good idea at the moment—especially for those looking to access negative gearing or avoid involving family in legal structures.”

Final Thoughts: Take It Case by Case

Structuring your investments properly is one of the most important financial decisions you’ll make as an expat. But the right structure depends on your income, your risk profile, your goals, and whether you're coming home soon.

“It's not just tax,” Tim reminds us, “it’s also about lending and what’s actually practical from offshore.”

What Do You Think?

Have you invested through a trust or company while living abroad? Was it worth it—or more trouble than it was worth? We’d love to hear your experience in the comments.

And if you're unsure whether a trust makes sense for your situation, reach out for a chat. We can connect you with the right tax and lending experts to guide the way.

.png)